Locate.

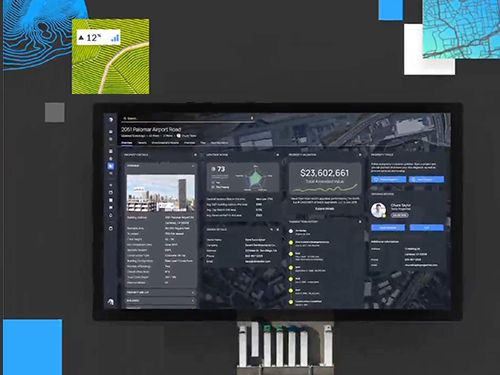

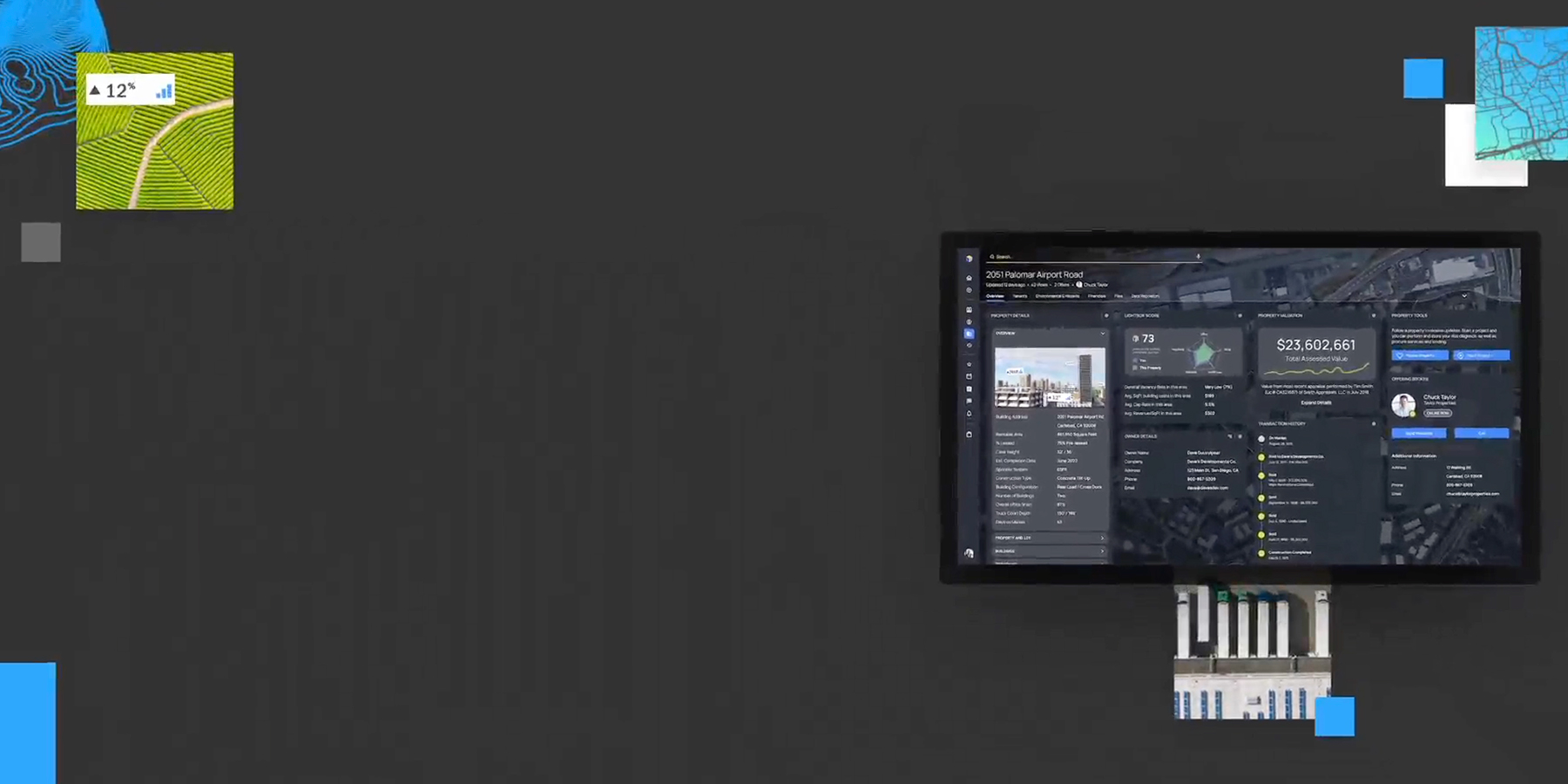

The most comprehensive set of property characteristics, tax parcels and building footprints, and spatial & environmental data.

Three simple words that empower decision makers in the commercial real estate market by delivering the most authoritative property data, integrated CRE workflows & unmatched industry connections.

The most comprehensive set of property characteristics, tax parcels and building footprints, and spatial & environmental data.

A deeper understanding of all facets of property data along with location intelligence and a simplified workflow to help you move forward.

Know you have the most comprehensive commercial real estate database and most detailed analytics so you can act on decisions with the highest degree of confidence.

From location intelligence to environmental due diligence to lending, valuation and broker resources, we offer solutions that deliver depth, speed and accuracy to help transform how you do business.

We unify and optimize the world’s broadest, deepest data sources — boundaries, neighborhoods, property and environmental — to ensure you can make every decision with confidence.

Our pioneering CRE solutions facilitate thousands of decisions daily across diverse industry sectors, including:

Let’s chat about your needs. Talk to support specialist or request a demo.

We provide solutions for customers ranging from the world’s leading mobile and web applications to government agencies and regional real estate developers. And we never stop seeking new ways to solve our customers’ unique challenges.

“We use LandVision℠ to better understand the market and identify micro-markets within. It enables us to drill into parcel level data that includes ownership information, zoning, date of last transaction, etc.”

CA Student Living

“Valuation uses an Excel-to-Word based process that connects to the online database platform to other tools, saving me at least four or five hours per appraisal. This frees up time for other things, from producing more reports for clients to spending more time with my family.”

![]()

Hutchinson Valuation, Inc.

“Having used Real Capital Markets® on several assignments, our team has been extremely impressed by the responsive service and quality of product produced by RCM®, as well as the increased target market provided by RCM’s extensive database of buyers. On a recent transaction that threatened to be extremely challenging, we generated 12 offers.”

Cushman & Wakefield

“If you want a commercial real estate CRM software that is ready to use today, use ClientLook®. You don’t have to do an elaborate build out or have any special training; you can be up and running quickly.”

![]()

CBRE

“Everything we do is property-related, and we get so much value from the data we gather from LandVision℠. I can’t imagine what businesses did before this type of technology solution was available.”

Anchor Loans

“In this heated capital environment, it’s only prudent to employ RCM®’s resources, especially since every buyer group is currently in play. I call it my ‘sleep at night’ marketing program, and it’s what I would use to sell my own property. I’ve employed RCM® successfully over the last couple of years and highly recommend it.”

Newmark

“LightBox Valuation helps me focus on a methodical and streamlined way of getting reports done. It’s a must-have business solution that helps me manage my appraisal process from start to finish and makes it easier for me to grow my company.””

Orr Appraisal

“ClientLook® is backed by some of the best people in the industry and was created specifically for commercial real estate professionals. If this is your industry, choosing ClientLook is a must.”

![]()

NAI Capital

“A big benefit is that we can track the complete holdings of an individual and can see what other properties they own. Being able to see everything together shows me what owners might be willing to do with their portfolio.”

SVN/Walt Arnold Commercial Brokerage, Inc.

“RCM® continues to turn out the Best in Class product when it comes to online property marketing. The quality of RCM’s teasers, online offering, comprehensive document library and buyer database is second to none, and has helped us to dramatically enhance our sales productivity.”

Fairfield Residential LLC

Discover how LightBox Labs harnesses the power of data and creative problem solving to pioneer innovative solutions within the industry.